Inflation persists as the Fed Chair’s term expires

Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

On Friday, May 15, the 10-year Treasury yield closed at 4.59%, its highest level since February 2025. The 30-year Treasury yield closed near 5.12%, a level last seen in 2007. Those are significant moves because they reflect a repricing of the market’s inflation, growth, and Federal Reserve expectations.

Inflation is the most visible driver, but it is not the only one. Recent inflation data has been hotter than investors wanted, energy prices have added pressure, and the market is increasingly questioning how soon the Fed can move toward lower interest rates. Long-term yields also reflect term premium, Treasury supply, and investor demand for compensation to own longer-maturity bonds.

Last week’s Producer Price Index (PPI) report reinforced those concerns. PPI measures price changes from the producer and business perspective rather than the consumer perspective. It matters because it can identify inflation pressure earlier in the supply chain. If businesses face higher input costs, they either absorb the hit through lower margins or pass some of the cost along to customers. The April PPI report showed final-demand prices rising 1.4% for the month and 6.0% over the prior year. Energy was a major contributor, but the breadth of the increase still caught the bond market’s attention.

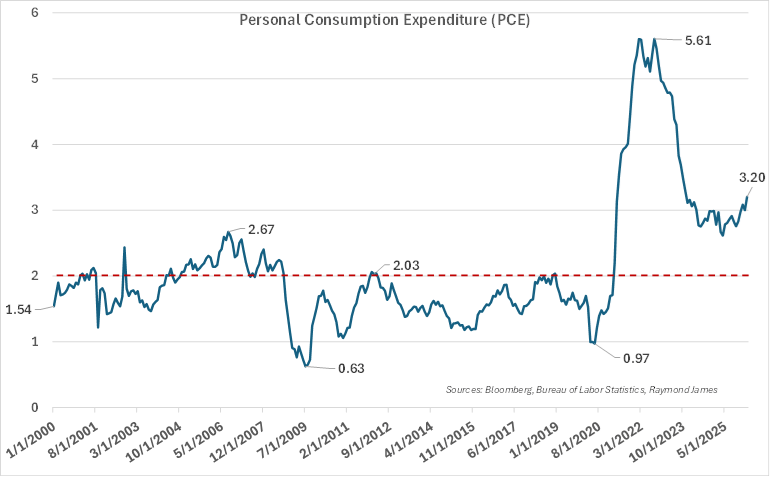

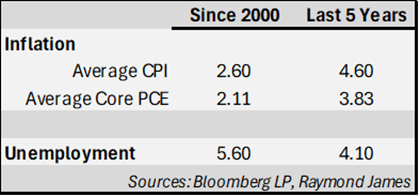

The Personal Consumption Expenditures Index (PCE), the Federal Reserve’s preferred inflation measure, has also moved in the wrong direction recently. March PCE inflation was 3.5% year over year, well above the Fed’s 2% target. That matters because the Fed is unlikely to cut interest rates aggressively while inflation remains above target and the economy continues to show resilience.

Friday also marked the end of Jerome Powell’s term as Fed Chair. His tenure will be judged in the context of an extraordinary period: the pandemic, emergency monetary stimulus, inflation’s surge, and the Fed’s later effort to restore price stability without causing a severe recession. The Fed’s balance sheet expanded from roughly $4 trillion before the pandemic to nearly $9 trillion in 2022. It has since declined to roughly $6.7 trillion, but it remains large by historical standards. Short-term interest rates also stayed near zero for an extended period, reflecting the Fed’s initial focus on employment and economic recovery before inflation became the dominant problem.

The practical question is whether the “soft landing” has truly been achieved. Inflation has come down from its peak, unemployment has not suffered a major long-term deterioration, and the economy has avoided a deep recession. But inflation remains above the Fed’s target, and the recent backup in long-term yields suggests the bond market is not yet convinced that the inflation problem is fully resolved.

For investors, this creates a real opportunity, but it should be framed carefully. Higher yields make high-quality bonds more attractive than they have been for much of the post-2008 period. Individual bonds can provide defined income, greater principal certainty when held to maturity, and portfolio stability relative to growth assets. For investors with long-term goals, known future cash needs, or a desire to reduce equity risk, today’s yields may be worth locking in.

That said, higher yield does not eliminate risk. Long-maturity bonds can still decline in market value if rates continue to rise. Credit quality, maturity selection, reinvestment risk, and the investor’s time horizon all matter. The opportunity is not simply “buy long bonds.” The opportunity is to build portfolios with income levels that were unavailable for many years, while matching maturities and risk exposure to each investor’s actual objectives.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.